Is greed responsible for the invention of Bitcoin?

A look at why Satoshi may have written his famous white paper

Hi Friends!

I hope you celebrated the Festival of Colours with friends and Family!

Three weeks and three articles! Let me start by welcoming our 9 newest subscribers. Our growth from 0 —> 39 subscribers and 0 —> 150 views per post, is slow but steady. I have so many ideas that I am working on. I can’t wait for you my readers to get the most out of cryptomallu! Please do share this article and let’s grow our community.

On 31st October 2008, a theoretical white paper was published by a pseudonymous person or persons called Satoshi Nakamoto, titled "Bitcoin: A Peer-to-Peer Electronic Cash System". To say that this paper was appropriately timed is an understatement.

In this article, I want to explore the events that led to this white paper. I will look back in history to understand our current economic framework and its dependence on banks and other financial institutions. What happens when these pillars of trust fail? How did we create this system that relies heavily on these institutions working effectively and constantly?

BRIEF HISTORY OF BANKING

In my previous article on the history of money, we learned how commodity money led to representative money, which required trusted third parties to make it work. These trusted third parties stored commodities like grain, silver, gold, etc. and gave warehouse receipts in exchange. Eventually, people started trading these receipts, relying on their underlying value. These warehouses and goldsmiths were the first bankers. A great example is the Egyptian grain-banking system. It functioned like a network of banks centred in Alexandria, where the main accounts from all Egyptian regional grain-banks were recorded. These grain-banks had several branches and handled a large volume of transactions.

Over time, banks started playing an increasingly important role in the economies of nation-states. They were able to create new forms of financial instruments like loans, lines of credit, cheques, etc. Cheques, for example, have been around in some form since the 1600s in England. Payments were settled by direct courier to the issuing bank or by the two banks meeting at a central location. Centralised clearinghouses were introduced by the 1800s.

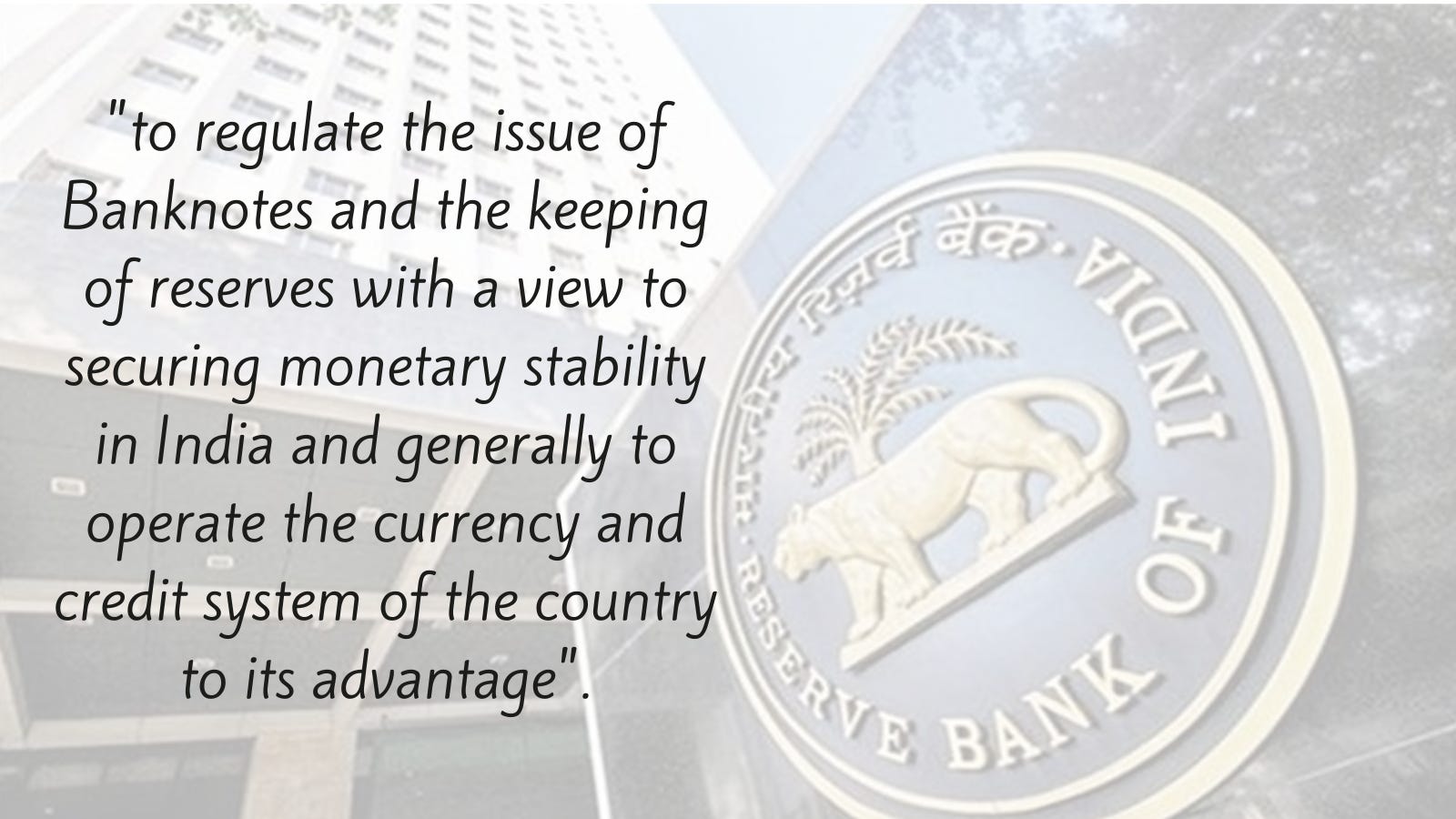

Due to the high volume and circulation of banknotes issued by commercial banks, many countries had to introduce regulations that restricted the issuance of notes by country banks. An example of this is the Bank Charter Act of 1844, in Britain, which institutionalised bullionism by creating a ratio between the gold reserves held by the Bank of England and the notes that the bank could issue. This effectively made the Bank of England a Central Bank.

The role of a Central Bank has been very nicely articulated in the preamble to the Reserve Bank of India, 1934 (the Act):

While Central Banks were responsible for printing notes and helping the government manage the economy, Merchant Banks continued to broaden their role. They delt in everything from introducing overdraft facilities to underwriting bonds. The number of such banks grew by leaps and bounds during the Industrial revolution and facilitated global trade growth. Especially in the U.S., these institutions made it so that money was readily available to investors riding the stock market boom of the early 1900s.

Unfortunately, there wasn't sufficient regulation in place to govern these institutions. The margin requirement of banks were as little as 10%, so when the crash of 1929 happened, debtors couldn't repay these loans. Over the next several years, thousands of banks failed, forcing many countries to significantly increase financial regulation, including separating investment banking and commercial banking. The idea was to avoid more risky investment banking activities from ever again causing commercial bank failures.

As America was reeling from the great depression, the world was going into war. The focus shifted towards the war effort. After the war, the banks again led the way with critical innovations and fueled growth. In the 50s, 60s and 70s, banks introduced the first automated reader-sorter machines for clearing cheques and the first ATMs to dispense cash. These innovations and a strong focus on automation helped banks reduce the need for sizeable clerical staff. This also enabled banks to introduce international electronic payment systems like SWIFT and other domestic payment networks. The 80s and 90s saw significant global banking and financial services growth, with several countries deregulating their financial markets. In the late 90s and early 00s, U.S. retail banks embarked on big rounds of mergers and acquisitions. They started engaging in investment banking activities again. With the adoption of the internet, the first decade of the 21st century saw a significant shift away from traditional banking to internet banking.

CREDIT & ITS ROLE IN MODERN SOCIETY

I was shocked to learn that credit is the primary form of money in most modern economies. It is believed that over 95% of funds in the United Kingdom is created as credit. But credit is not just limited to loans provided by banks. Think about it, most businesses exchange goods and services on credit. This is especially true in B2B transactions. Previously, I have mentioned how credit and debit function effectively only if trust and regulation are in place. Did you know that credit comes from the Latin word credit and literally means "(he/she/it) believes"!

Time to reintroduce Bill and Ted, who will show us how credit works! Credit is essentially the trust which allows farmer Bill to provide grain to Ted, wherein he doesn't get reimbursed immediately (thereby generating a debt). Instead, Ted promises to repay at a later date.

Banks create two primary forms of private credit

Unsecured Credit

Secured Credit

UNSECURED CREDIT

The most popular form of unsecured credit is everyone's favourite Credit Card. When the bank is extending the credit purely on trust and has no collateral if you default, it is called Unsecured Credit. Understanding the distinction between your favourite credit card network and your bank is essential. Companies like VISA, Master Card, Diner's Club and American Express have created extensive payment networks that link merchants with banks. The Credit Card itself is actually provided by your bank. The credit limit set by them is based on your personal creditworthiness.

Banks also provide small unsecured loans to their customers based on their creditworthiness. How this creditworthiness is determined is a whole different article (one I will write if any of you guys are interested in - )

In general, because the risk to the bank / financial institution is much higher, they tend to charge a significantly higher interest rate on Unsecured Credit.

SECURED CREDIT

Credit extended to an individual or entity against collateral is called secured credit. Most often, the collateral is the item being purchased. When banks and financial institutions loan out large amounts of money or extend significant credit, it is necessary to reduce the risk exposure. Your creditworthiness is the first and most important parameter. Still, when the amounts are large, they will also require collateral, something of equivalent value to the loan.

Because of the reduced risk, the interest charged will generally be lower than is the case with Unsecured Credit.

WHY IS THIS RELEVANT?

I am getting into the weeds with this stuff because it is essential to understand the critical role that Banks and Financial institutions play in our day to day lives. The trust and dependence in these banks and financial institutions have helped humanity. Having created vast, complex networks to safeguard and transfer money, they enable global trade and commerce. Nation-states have understood their importance and tried to put necessary regulations to ensure that they can't break our trust. However, there will always be bad players when so much money is involved. Sometimes an entire ecosystem of such institutions could turn a blind eye to poor financial models.

The 2008 global financial crisis is one such example. I won't try to explain how it came about, but I will summarise based on this fantastic article by Investopedia. A combination of cheap credit and poor lending standards fuelled the crisis. This is different from the great depression of 1929, where banks and financial institutions extended too much-unsecured credit that investors in the equity markets. Investors couldn't repay when the markets crashed, leading to bank failures and depression.

Post the I.T. bubble bursting in 2001, the U.S. Fed reduced interest rates to 1%, fuelling a sudden increase in new home buyers. The housing boom was so intoxicating that financial institutions even lent money to individuals with poor creditworthiness. These loans were called subprime loans. Eventually, when the market was saturated with homeowners and the demand began to reduce, the value of homes started to slide. Very soon, the price of the house was lower than the loan repayment amount.

Unlike in the past, the whole world was affected by this crisis because everything is now linked together. Debtors began to default, and soon, the very financial institutions that we trusted to manage our money didn't have enough cash to repay their customers. Many global financial institutions were equally involved in the subprime crisis. The Northern Rock Building Society, based in Newcastle, England, was the first large financial institution to fail in August 2007 and had to be bailed out and Nationalised by the British government. In March 2008, Bear Sterns, an 80+-year-old financial institution and pillar of Wall Street, announced bankruptcy and was bought by JP Morgan Chase. The final straw was the Wall Street bank Lehman Brothers declaring Bankruptcy in September 2008. It marked the largest bankruptcy in U.S. history.

The Wall Street bailout package was approved in the first week of October 2008. Though economists believe that this was the only move that the U.S. Government could make at the time, there was a significant public backlash. The term "too big to fail" became part of public discourse.

{kind=link}

{kind=link}

These events and the general mistrust in financial institutions may have resulted in the now-famous white paper by Satoshi Nakamoto on 31st October cryptography mailing list at metzdowd.com describing a digital cryptocurrency. Future articles will explore this white paper and its implications.

I hope my articles so far have played a role in laying the foundation necessary to help us better understand the world of cryptocurrency. This one, in particular, took a bit of time to workout and structure in a manner that made sense to me. I hope you enjoyed it! Until next week!

Some housekeeping: Initially, I shared my articles on Sunday morning at 8 am. But most of you don't check your emails over the weekend (a good thing). So going forward, I will be posting on Monday mornings at 8 am.